That is half 2. Take a look at half 1, MEV resolutions: Are we there but?

As we mentioned final month, the MEV ecosystem is rising quickly. As a substitute of making an attempt to clear up MEV, focus has shifted to incorporating it into software and protocol design. MEV mitigation and democratization have grow to be an important issues in DeFi (and arguably, all of Ethereum). But whereas MEV mitigation efforts are essential to make Ethereum straightforward to make use of, the options rising over the previous yr (whereas aggressive), have come on the expense of decentralization.

This has led to soul looking out over the true aim of the DeFi ecosystem. Is it creating merchandise which might be aggressive with TradFi and centralized crypto exchanges? Or is it attaining some undefined decentralization finish level?

This debate is finest exemplified by the latest rise so as move auctions (OFAs), the MEV mitigation technique that returns the worth extracted again to the top consumer (for a price).

There are numerous totally different options within the works (and we focus on the primary ones afterward), however all of them observe the identical sample:

-

Order routing and execution are delegated to specialised networks exterior of Ethereum.

-

This intermediate computation layer depends on trusted actors to mediate between customers and validators.

-

These new networks empower refined (and centralizing) market makers, however this comes on the expense of on-chain liquidity.

Is non-custodial buying and selling with skilled market makers inevitable for DeFi? Decentralizing the MEV provide chain and democratizing MEV rewards are hurdles to clear, however this won’t be the catalyst of latest progressive DeFi merchandise that conquer CeFi and TradFi.

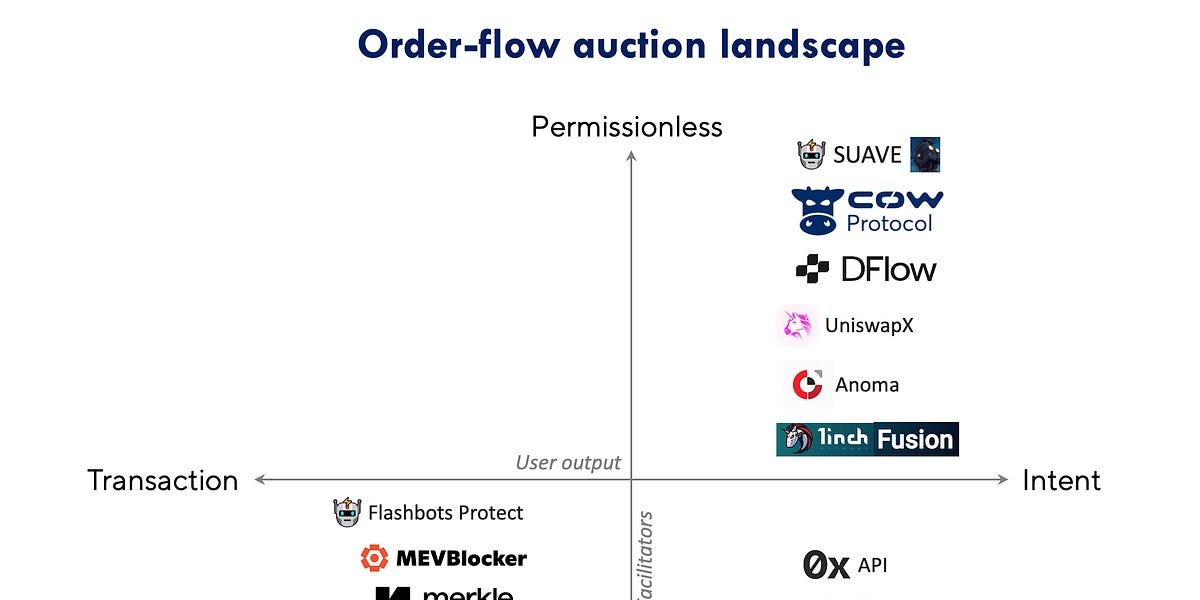

Let’s first do a inventory tackle the newer strategy to MEV mitigation. Over the previous yr, there was an enormous shift in how DeFi customers commerce on Ethereum. More and more, they’re sending their trades to not the general public mempool however to non-public networks that fill and execute orders and return a portion of the MEV extracted again to customers. These OFAs, the place searchers/solvers/fillers bid on the precise to execute orders utilizing each on and off-chain liquidity, are available in all styles and sizes

These networks function trusted (for now) intermediaries. On one facet are retail customers and the opposite is a set of market makers, bidders, searchers or solvers, which we’ll discuss with as facilitators. Shifting order routing off-chain to facilitators yields a big gasoline price financial savings, whereas customers get higher costs as a result of facilitators may also use off-chain liquidity. Facilitators may theoretically commerce in opposition to their customers (frontrun or sandwich) however this might jeopardize their future move. So, it’s in the very best curiosity of the OFA networks to make sure facilitators should not performing maliciously.

OFAs have alternative ways of policing facilitators. Some solely enable sure entities to bid for order move (permissioned), whereas others enable anybody to take part however can retroactively punish dangerous actors (both by slashing a stake or simply banishing them from the community). Others enable facilitators to bid for orders permissionlessly by utilizing a batch (CowSwap) or Dutch public sale (Uniswap X, DFlow, and 1inch Fusion). This requires extra time for the public sale to finish and the OFA community should nonetheless belief that the block builder is just not extracting MEV when it passes alongside the transaction bundle to validators.

There’s now a feverish rush to redirect all retail move from the general public mempool to non-public OFA networks. Uninformed retail merchants are the supply of MEV, so anybody that controls that move can entice the very best facilitators and market makers to their community. OFA networks are concentrating on wallets and RPC suppliers, in addition to constructing their very own front-ends. A number of distinguished organizations have launched their very own personal mempools, like Blocknative’s Transaction Enhance, Flashbots Shield, and MEV Blocker (from Gnosis). In the meantime, various impartial transaction-based personal mempools, corresponding to Merkle and Kolibro, have just lately emerged. Proudly owning retail move is an important a part of the MEV provide chain.

In evaluating the rise of those OFA networks, we additionally want to recollect a key differentiator: between these whose enter is the consumer’s transaction, versus these which might be a consumer’s intent. Intent is a made-up time period – crypto is excellent at that – to explain a consumer’s want for a sure end result, relatively than a transaction, which is particular traces of code to execute. Flashbots’ Quintus Kilbourn and Paradigm’s Georgios Konstantopoulos outline it succinctly:

If a transaction explicitly refers to “how” an motion ought to be carried out, an intent refers to “what” the specified end result of that motion ought to be. If a transaction says “do A then B, pay precisely C to get X again”, an intent says “I would like X and I’m keen to pay as much as C”.

For many customers excited by executing a swap at the very best worth with the bottom charges, utilizing an intent-based structure is good. Most customers don’t care how their order is executed, solely that whoever executes it abides by circumstances outlined by the consumer.

This harkens again to the traditional debate on whether or not blockchains are finest regarded as a world pc or a worldwide settlement layer. Clearly, there are advantages to good contracts and trustless execution, however at what price? It additionally suits into the development of shifting execution to Layer 2s typically. The distinction being that when utilizing Arbitrum or Optimism, you might be utilizing the identical execution engine as Ethereum (the EVM) and posting a proof of the execution on Ethereum. OFA networks and intent-based blockchains (like SUAVE, Anoma, or DFlow) can even want to supply comparable belief assurances, in the event that they need to preserve the identical belief assumptions as execution on Ethereum.

Efforts to mitigate the detrimental externalities of MEV by way of OFA networks have had one apparent casualty: on-chain liquidity. All efforts to route trades to non-public OFA networks imply that facilitators have the primary have a look at filling orders. Facilitators can faucet into liquidity supplied by on-chain automated market makers like Uniswap, Balancer, and Curve, however they’ll solely get move when facilitators resolve it’s not price utilizing their very own liquidity. On-chain liquidity suppliers are already getting slammed by CEX-DEX arbitrage and issues from loss versus rebalancing (LVR), however within the new market structure to reduce MEV, they can even forfeit their unique entry to retail DEX merchants.

So, are on-chain liquidity and MEV mitigation actually mutually unique? Not everybody thinks so. Present efforts to reduce MEV extraction whereas nonetheless empowering on-chain liquidity suppliers (LPs) are underway. The best methodology is to return MEV from CEX-DEX arbitrage again to LPs. The method goes like this: A worth change on Binance results in a rush to commerce in opposition to Uniswap LPs that haven’t but included the brand new worth. There’s an enormous quantity of worth to be extracted from whomever will get to commerce in opposition to the LPs first. The McAMM (MEV capturing AMM) design would public sale off the precise to the primary commerce per block and return the proceeds to LPs.

Empowering LPs can be the muse for Uniswap v4 and Ambient Finance, which we referred to as “Recent hope for passive LPs” in a deep dive in June. Each of those AMMs allow swimming pools to be programmed with “hooks”. The design house for these has not but been totally explored (Ambient launched in June and Uni v4 has but to completely launch), however they may impose restrictions on who can commerce with a liquidity pool. Theoretically, they may solely enable trades from sure OFA networks or personal mempools. This implies retail move could possibly be aggregated and solely given to particular Uniswap/Ambient LP swimming pools. Extra importantly, hooks could possibly be designed to guard LPs from poisonous move but it surely additionally may restrict arbitrageurs rebalancing the pool. Just some weeks in the past, Arrakis launched Diamond Hook, a Uni v4 hook meant to alleviate LVR issues for LPs, though some query whether or not it might obtain its mission.

The efforts to resolve the MEV disaster are rejiggering the whole DeFi panorama, so it’s price taking a step again to ask, what are we making an attempt to realize? We’ve been writing about DeFi for nearly 5 years due to the earnestness of these working in it to construct a greater monetary system (regardless of a scarcity of consensus on what this really is!)

To us, DeFi has three worth propositions that make it a monetary system that conceptually doesn’t enshrine market winners as long-term hire extractors:

-

DeFi is clear. FTX couldn’t occur on-chain as a result of DeFi is non-custodial. BlockFi couldn’t occur in DeFi as a result of the mortgage ebook is open and liquidations are computerized.

-

DeFi is international first. Nationwide regulators can limit entry on the software layer, however DeFi’s default setting is open entry all over the world.

-

DeFi unlocks new monetary merchandise and improvements by means of programmable cash and creates an open platform for others to permissionlessly construct on prime of, very similar to the web.

Does the current MEV provide chain preserve these ideas? It’s too early to inform, however there are some crimson flags. OFAs don’t (but) supply the identical transparency as on-chain execution. Facilitators have gotten extra refined and it’s attainable that we’ll find yourself in a world the place fillers/solvers/searchers are all giant Wall Avenue market-making corporations. This isn’t inherently a foul factor, however trade focus makes it a straightforward goal for regulators and threatens DeFi’s international nature.

As for unlocking new monetary merchandise and innovation, OFAs are targeted on finest execution and the present construction appears an terrible lot just like the one Robinhood and Citadel already pioneered.

Even when this grew to become the top state for DeFi, three big improvements would nonetheless have been unlocked:

-

Non-custodial buying and selling: The unique motivation for creating decentralized exchanges was to permit customers to keep up management of their crypto and shield in opposition to the chance of hacks, inside jobs, and self-dealing at centralized crypto exchanges. An intent-based DEX settled on Ethereum fulfills that imaginative and prescient.

-

Bootstrapping liquidity for long-tail property: Even when refined market makers are the first liquidity suppliers for blue chip property, on-chain AMMs are nonetheless one of the best ways to bootstrap liquidity – and a useful innovation for the long-tail of property. These round in pre-Uniswap instances will bear in mind how exhausting it was to construct a liquid market on primitive DEXs like Ether Delta. Permissionless on-chain liquidity swimming pools are an infinitely higher choice than the shady enterprise practices of CEX listings.

-

On-chain lending swimming pools: The lending facet of DeFi has not been as obsessive about MEV as DEXs. Whereas there are points to beat (particularly round oracles), on-chain credit score markets are simply getting began, and have continued to provide new, fascinating merchandise even within the bear market.

Plenty of promising MEV mitigation methods are rising, however what finally wins out is much less necessary than shifting previous MEV as the focus of DeFi. The important thing consideration for any blockchain’s MEV ecosystem is whether or not MEV extraction or redistribution threatens the three DeFi worth propositions we outlined above. Centralizing components within the MEV provide chain will imperil all three.

So who’s doing it properly? dYdX and the Cosmos ecosystem are utilizing the appchain mannequin and on-chain governance to make sure that their validators should not extracting MEV – or at the least are clear about it. This implies the chains can keep targeted on constructing nice DeFi merchandise. Skip Protocol is a sovereign MEV infrastructure supplier underpinning a lot of the advances within the Cosmos MEV ecosystem.

The rise of OFAs is a essential step in defending DeFi customers in opposition to the risks of the darkish forest. We’re most inspired by SUAVE, Flashbots’ new blockchain (set to launch a Devnet in This autumn), as a result of it gives higher transparency in execution, privateness safety, and a reputable path to decentralizing block manufacturing. Decentralized sequencers for Layer 2s, like Espresso or Astria, should not too dissimilar.

In the end, we drink the kool-aid on intent-based programs, and suppose the delayed public sale format utilized by CoW, Uniswap X, DFlow, and 1inch Fusion is the very best market construction to forestall centralization of facilitators whereas remaining permissionless. Transparency in intents execution continues to be sorely wanted.

Decentralized OFAs won’t be sufficient to beat CeFi. New primitives are wanted. Essentially the most promising growth in MEV mitigation and DeFi innovation extra broadly is the brand new DEX design of Uniswap v4 and Ambient Finance. These are the primary DEXs to be designed with MEV mitigation methods. The idea of “hooks” permits LPs to discriminate between poisonous and non-toxic move, which may lastly generate optimistic returns for LPs.

Many DeFi customers had been turned off by the rise of MEV because of the fixed concern of getting taken benefit of. This rightly drove analysis into mitigating issues for the common consumer. The all-encompassing nature of MEV has made it really feel like the one recreation on the town. It’s extremely necessary to repair, however new sorts of MEV extraction and redistribution received’t be what drives innovation in DeFi, nor what makes it profitable long run. The important thing to any MEV answer have to be one that enables for DeFi to return to its roots: a clear, international monetary system the place entrepreneurs can construct new monetary merchandise which might be unlocked by means of good contracts and programmable cash.

To place our playing cards on the desk, we strongly consider that DeFi will solely work long run if there may be transparency in how orders are executed, and if retail customers can earn some optimistic return by LPing. After all, refined actors ought to be capable to earn a better return, however DeFi may have failed if it might’t produce greater than an up to date model of an on-chain index fund. Others contend that “passive LPing will [never] be worthwhile” and the aim is to merely return worth leaked to LPs to make wholesome markets on-chain. On this world, the charges usually paid to Blackrock could be paid to rebalancers within the MEV ecosystem. So DeFi is having your ETF managed by a decentralized market of merchants settled on a blockchain.

These are totally different visions for the way forward for DeFi, and now that MEV mitigation and redistribution methods are in place, we are going to see which one wins out. Our take:

-

PoolTogether launches v5 Hyperlink

-

Ethereum basis will get $9k extracted on on-chain ETH commerce Hyperlink

-

Ethereum mempool transactions now on Dune Hyperlink

-

Elixir, DeFi protocol aimed to extend orderbook liquidity, raises $7.5m Hyperlink

-

Over $500k in cumulative price income for Uniswap labs from front-end price Hyperlink

-

USDC provide dropped 44% since ATH to $23bn Hyperlink

That’s it! Suggestions appreciated. Simply hit reply. Particular because of Daniel MacLennan for dialogue and suggestions on immediately’s publish. Written in Nashville. Comfortable fall y’all.

Dose of DeFi is written by Chris Powers, with assist from Denis Suslov and Monetary Content material Lab. All content material is for informational functions and isn’t supposed as funding recommendation.

{kind=link}