On Monday, the Senate voted 66-32 to invoke cloture on the GENIUS Act, a invoice that regulates the creation and providing of stablecoins within the US. Whereas the invoice nonetheless must clear the Home and be signed by President Trump, passing the Senate was the most important problem (on condition that it required Democratic help to hit the 60-vote threshold for cloture). With that hurdle cleared, the GENIUS Act is now on observe to turn into the primary piece of crypto laws handed by Congress.

It is ironic that the first-ever crypto laws enshrines fiat currencies into the material of blockchains. This can be a far cry from the early crypto days the place fiat was the enemy, and the separation of cash and state was the objective. Quick ahead, and now US politicians are speaking about how blockchains might additional the dominance of the USD.

How did we get right here? And the place are we headed subsequent? With stablecoins now set to be enshrined in regulation, crypto’s journey from aspiring anarchist cash is pointing squarely at its true vacation spot: stateless monetary infrastructure.

Within the early days of Bitcoin and crypto, there was a typical sentiment among the many fits of Wall Road: they had been within the underlying know-how of Bitcoin (blockchains) greater than in Bitcoin the foreign money. Some even began what they referred to as “enterprise blockchains”, whereas others dropped the blockchain moniker altogether and mentioned they had been constructing “distributed ledger know-how”.

None of these efforts succeeded at attracting utilization and had been typically scoffed at by these within the Crypto business (and never simply Bitcoiners), as a result of they weren’t permissionless or decentralized. The fits of Wall Road believed {that a} risky foreign money was not going to turn into the inspiration of a brand new monetary system, and ultimately us crypto bros figured it out. As we highlighted in (my favourite) Dose of DeFi in February 2020:

There’s a typical trope the place a Bitcoiner – usually an American male – admonishes an inflation-ravaged nation and preaches the gospel of Bitcoin and its mounted provide. From his snug perch on Twitter, he speaks of how Bitcoin is the answer to a growing nation’s woes, if solely the folks would admire laborious cash and Austrian economics.

To this point, Bitcoin has not been a savior to any economic system. Its censorship resistant P2P funds have given people in repressed regimes an vital lifeline, however it has not been adopted at scale in Venezuela, Zimbabwe or different inflation-challenged international locations.

We thought they needed Bitcoin, however possibly it was simply the US greenback?

Ultimately, ideological skirmishes gave approach to market demand. The quiet utility of dollar-backed tokens on blockchains proved to be the pragmatic path for adoption.

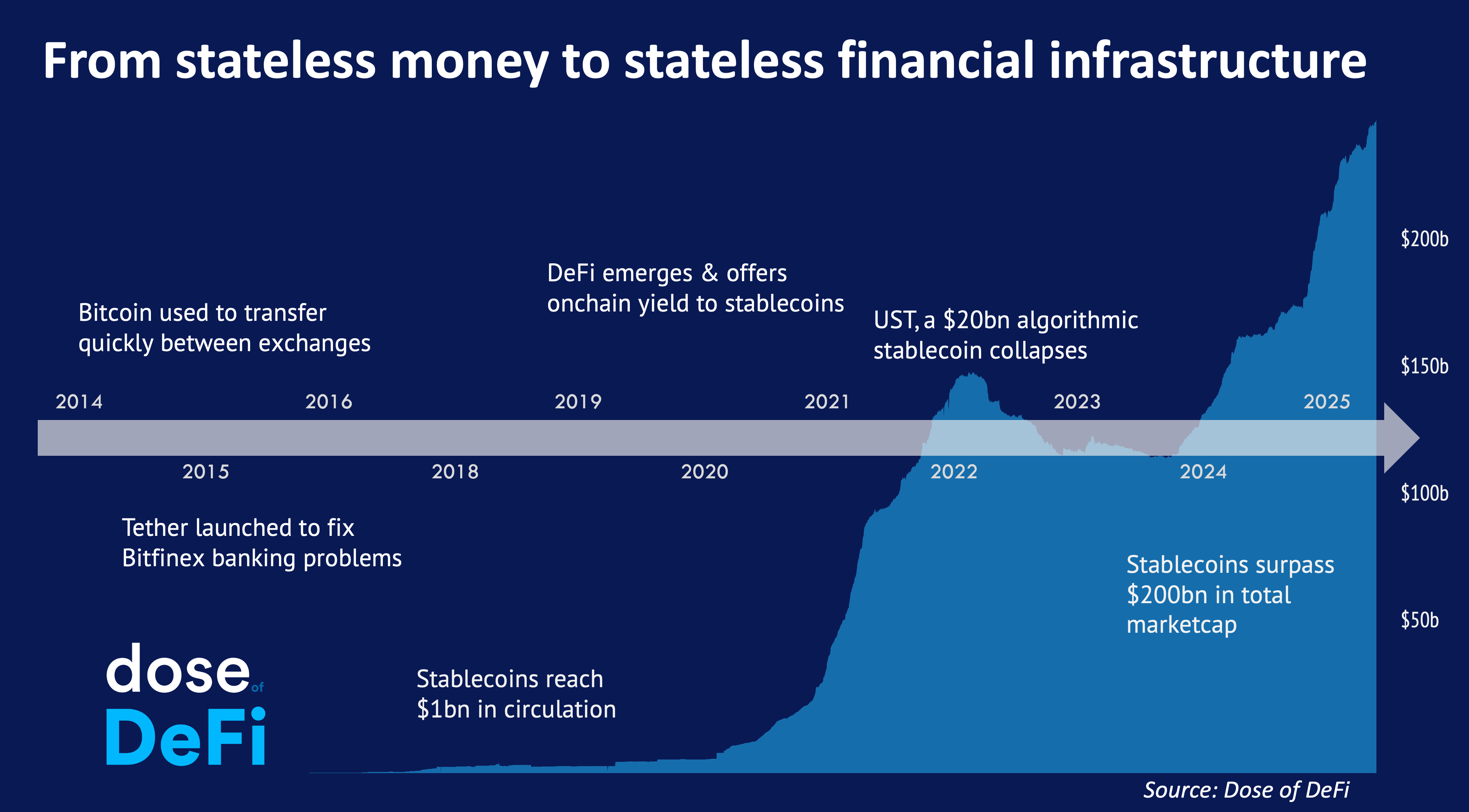

So, it appears crypto’s adolescent desires of overthrowing the financial order have largely pale (for now), changed by the extra sober actuality of its basic position as monetary infrastructure. Early Bitcoiners had been hyper centered on making the cash angle work, however ultimately, there have been no takers (sin El Salvador). Folks, because it seems, had been much less fascinated about a brand new foreign money and extra fascinated about utilizing these novel blockchain rails to maneuver good outdated US {dollars} across the globe, effectively and rapidly.

This proved significantly useful within the often-clunky world of crypto exchanges as Bitcoin professionalized after the 2013 bubble. Initially, Bitcoin itself served this goal: you may withdraw it from one alternate and deposit it into one other, sidestepping the ponderous financial institution wire system so long as each platforms supported BTC. Then got here Tether (USDT), providing an improve by eradicating the pesky foreign money threat inherent in utilizing Bitcoin as a bridge asset. Why gamble on Bitcoin’s value swings whenever you simply needed to maneuver worth?

A couple of years later, after the 2017 ICO bubble created property onchain and hundreds of ERC-20 tokens, new DeFi buying and selling and lending protocols launched, including one other layer of validation for blockchains (as genuinely-useful monetary plumbing). It quickly grew to become obvious that crypto’s hottest product – leveraging-up to purchase extra crypto – solely works in case you can borrow in a secure foreign money. These new DeFi lending platforms supplied the primary onchain yield for stablecoins, and in doing so, broadened their attraction past merchants to anybody merely seeking to save in {dollars}, particularly in the event that they had been outdoors the normal US monetary system.

It’s vital at this level to keep in mind that this wasn’t some grand, orchestrated plan by the US authorities. Nobody informed Bitfinex to make use of a USD stablecoin to resolve their banking issues. Justin Solar wasn’t appearing on a State Division memo when he used greenback stablecoins for his playing apps in rising markets. And nobody from the Treasury informed Uniswap to improve its v2, which newly enabled any asset to be paired with stablecoins, not simply ETH. This was uncooked, unadulterated market demand. Blockchains proved to be remarkably environment friendly monetary rails, made infinitely extra helpful by permitting the world’s reserve foreign money, {dollars}, to circulate by means of them.

This natural, market-driven gravitation in direction of US greenback stablecoins is exactly what jolted lawmakers into motion. There’s all the time been chatter about crypto regulation, oscillating between suffocating overreach and a dangerously gentle contact. However the stablecoin invoice managed to cross the end line as a result of the standard crypto advocates discovered unlikely allies, like Senator Mark Warner (D-VA):

The stablecoin market has reached practically $250 billion and the U.S. can’t afford to maintain standing on the sidelines. We want clear guidelines of the street to guard shoppers, defend nationwide safety, and help accountable innovation. The GENIUS Act is a significant step ahead.

So, to recap: crypto’s massive experiment as a brand new type of cash largely belly-flopped. However as monetary infrastructure? It has discovered its footing, sarcastically by hitching its wagon to the very US greenback it as soon as sought to supplant. The explosive progress of stablecoins compelled the legislative hand, however this invoice is not designed to kill stablecoins. It is the alternative. It’s a legitimization, a welcoming committee ushering stablecoins from the shadowy corners of Degenistan into the brightly lit, compliance-polished plazas of Wall Road and the meticulously-curated walled gardens of Silicon Valley.

Now again to the GENIUS Act, which is not nearly regulating some area of interest crypto asset. It is laying the groundwork for a rewiring of US monetary plumbing, with stablecoins on the middle. Whereas there are short-term aggressive dynamics for current stablecoins, the long-term implications are broad, touching all the things from how we pay for issues, to the very construction of banking.

Funds and the Stripe check: Probably the most instant impression will likely be on funds, and we’re already seeing main gamers dip their toes in. Stripe, the chief in on-line fee processing, has rolled out stablecoin-powered monetary accounts – initially supporting USDC – concentrating on companies globally. It additionally acquired Bridge, a stablecoin infrastructure firm, which allows some clean DeFi onboarding experiences. Visa and Mastercard are additionally within the sport, enabling shoppers to spend stablecoin balances by means of their current card networks, by partnering with issuers and pockets suppliers.

Financial institution disintermediation and the rise of ‘slim banking’: That is the place issues get actually attention-grabbing (and probably uncomfortable for conventional banks). If stablecoins turn into a most popular approach to maintain and transfer {dollars}, particularly for companies and digitally-savvy shoppers, what occurs to financial institution deposits? The normal banking mannequin depends on deposits to fund lending. If a major chunk of these deposits strikes into stablecoins, held in digital wallets or on platforms like Coinbase, banks might discover themselves disintermediated.

The reality is, banks are type of already disintermediated relating to lending. Sure, sure, they do a variety of small enterprise and mortgage lending, however specialised mortgage lenders typically originate these loans, that are then funded by bigger banks from their stability sheet. In a brand new world, these mortgage lenders would companion with funding funds which can be specialised in evaluating mortgages (or any mortgage). And so, we unbundle right into a mortgage originator after which an investor. When you squint, this seems to be like what the big debt markets are actually, each public bonds which can be freely traded and personal credit score, which is so sizzling proper now. This shift towards what economists name “slim banking” – the place monetary establishments take deposits however make investments them primarily in protected property like treasuries reasonably than making loans – is being accelerated by stablecoins.

But this future could also be a methods off, as a result of the banking foyer was capable of insert a provision within the GENIUS Act that prohibits interest-bearing stablecoins. Whereas the intention is prone to mitigate threat, the demand for yield is a robust power. We are able to anticipate that curiosity will nonetheless ‘leak out’, probably to much less regulated, non-US based mostly platforms and merchandise, much like how Aave charges can spike as a consequence of methods like looping Ethena’s USDe, or the emergence of choices like Sky Financial savings Price. If these exterior platforms turn into vital, this might ultimately create new systemic dangers for the US monetary system, forcing regulators to play catch-up with stablecoins as soon as once more.

Big new alternatives in DeFi (and the query of your subsequent mortgage): So, if banks aren’t the first supply of credit score, the place will you get your mortgage? Or your small enterprise mortgage? Enter DeFi. Our hope is that DeFi can step in to make this evolving credit score system extra clear and environment friendly. We do not have to make use of banks to increase credit score; we achieve this now inside a closely regulated market construction designed to make sure stability. DeFi protocols already supply avenues for yield by means of lending and liquidity provision. Think about a future the place your mortgage is not funded by a financial institution however by a DeFi protocol, funded by a worldwide pool of stablecoin liquidity. Yield-bearing stablecoins like BlackRock’s BUIDL fund or Ondo Finance’s OUSG supply a glimpse. These merchandise present compliant entry to yields from conventional property like US Treasuries, typically for institutional and accredited traders. May comparable buildings be tailored for broader client lending? This might create a vibrant, although probably riskier, panorama for credit score. A brand new order with much less credit score intermediated by means of banks may be higher, however we have to tread very fastidiously.

Whereas after all the instant implications of the invoice lie inside US borders, it additionally crops a seed for a shift within the position of the USD world-over. The opposite irony of the rise of stablecoins is that Tether, (by far) the most important US greenback stablecoin, is domiciled outdoors the US. Whereas Tether complies with all US regulation enforcement requests relating to KYC/AML legal guidelines, its founders have been skittish about coming into the US.

And whereas American politicians are centered on what occurs to Americans, the GENIUS Act can have a good larger impact on the remainder of the world. Whereas for the US, stablecoins’ legitimization will result in a change in market construction for credit score dissemination (that’s a giant transfer!), for the remainder of the world, it can problem the monopoly of native currencies. This isn’t nearly finance; it’s about financial sovereignty.

The dynamics right here about native monopolies collapsing remind us of Ben Thompson’s Aggregation Idea for media. It’s enjoying out once more, however this time with cash. When distribution prices for information collapsed because of the web, most metropolis papers withered and died, whereas giants like The New York Instances went world. The web rewarded the most important, most trusted model.

The identical dynamic is about to hit fiat currencies. Residents, particularly in international locations with unstable economies or restrictive monetary methods, will more and more choose USD-denominated stablecoins as a result of they’re perceived as extra secure and supply entry to world commerce. Governments, naturally, have a propensity to limit them to guard their very own financial management, however can they actually? Community results are highly effective.

This runaway success story for US greenback stablecoins hinges on a vital assumption: that the US desires to stay the worldwide reserve foreign money, and that elevated dollarization is definitely good for the American folks. The Trump administration, curiously, appears to assume in any other case, actively attempting to de-dollarize the world with the so-called Mar-a-Lago Accords. It’s not completely clear what their endgame is, or how Individuals actually really feel about this.

However simply take a look at the latest leap in US Treasury yields because the Trump administration’s rhetoric spooked overseas traders from holding treasuries. Decrease world demand for {dollars} and treasuries would not simply imply extra fiscal complications for the US authorities; it interprets to larger mortgages and automobile loans for on a regular basis Individuals. So, whereas the crypto world is busy constructing on-ramps for world USD stablecoin adoption, the query stays: is that this actually the specified end result for the US itself? The GENIUS Act may formally be about regulating stablecoins, however it’s inadvertently supercharging a a lot bigger home dialog concerning the greenback’s future position.

Whereas crypto is shifting onto stablecoins and stateless monetary infrastructure, it can by no means absolutely abandon its dream of financial sovereignty.

Bitcoin has undoubtedly achieved stateless cash. It marked one other all-time excessive this week and nonetheless has a protracted approach to run as digital gold (even when it’s not toppling dictatorships). Different types of stateless cash will probably emerge. Some would argue – and we’d agree – that Ethereum has reached that degree exactly as a result of it’s such a core stateless monetary infrastructure for thus many stablecoins and RWAs. Solana might get there as properly, however all crypto property that obtain stateless cash standing will achieve this each by means of payment technology – or REV because the cool children name it – and a financial premium that’s the collective perception in the way forward for the community by tokenholders – hey, not so completely different from Jay Powell’s common pep talks for the greenback.

However what’s crystal clear after the passing of the GENIUS Act is that stateless cash can even should compete with state cash that runs on blockchains, which is able to use their current community results to bid for supremacy in an age of stateless monetary infrastructure.

Gnosis launches v2 of Circles, a brand new group foreign money Hyperlink

Mixed metrics for monitoring good contract networks Hyperlink

Lido proposes twin governance construction improve Hyperlink

Trump memecoin holders prep for personal dinner reward: ‘I’ll put on a swimsuit’ Hyperlink

Fluid struggles with impermanent loss after massive ETH transfer up Hyperlink

New draft market construction invoice launched by Home Republicans Hyperlink

DeFi Llama is now monitoring threat curators by TVL Hyperlink

That’s it! Suggestions appreciated. Simply hit reply. Had a good time scripting this. Feeling optimistic about DeFi!

Dose of DeFi is written by Chris Powers, with assist from Denis Suslov and Monetary Content material Lab. I spend most of my time contributing to Powerhouse, an ecosystem actor for MakerDAO/Sky. A few of my compensation comes from MKR, so I’m financially incentivized for its success. All content material is for informational functions and isn’t supposed as funding recommendation.

{kind=link}