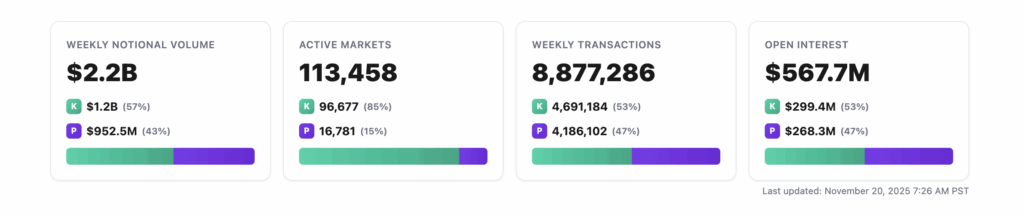

Kalshi constructed $1.2B in weekly quantity with US customers alone. Polymarket constructed $952M with everybody else, per Defi Charge analytics.

Kalshi has raised $1 billion in new funding at an $11 billion valuation, per TechCrunch. The spherical, led by returning buyers Sequoia and CapitalG, comes lower than two months after the prediction market operator closed a $300 million spherical at a $5 billion valuation.

The fundraise arrives alongside a notable information level: Kalshi now generates extra weekly buying and selling quantity than Polymarket, regardless of having constructed its consumer base nearly solely with American merchants.

Geographic context issues

Polymarket was barred from serving US residents from 2022 till September 2025. Throughout that three-year interval, the platform constructed its liquidity with merchants from Europe, Asia, and elsewhere.

Kalshi, in contrast, operated as a US-only trade till October 10, when it introduced enlargement to 140 nations. That enlargement is six weeks outdated, and per Sportico, worldwide entry stays inconsistent. Merchants in India, Brazil, Nigeria, and Finland have posted on Discord and X that they can not register accounts.

It’s truthful to imagine Kalshi’s present quantity is predicated on US customers.

This reframes the comparability in two methods. First, the US alone is producing extra prediction market exercise than the remainder of the world mixed—a testomony to American urge for food for occasion buying and selling. Second, Kalshi captured that market whereas Polymarket was locked out of it.

Per-market liquidity nonetheless favors Polymarket

The combination numbers obscure a big hole in particular person market depth. Polymarket’s highest-volume contract—Tremendous Bowl Champion 2026—has generated $160.7 million in buying and selling quantity over the previous 30 days. Kalshi’s main market, the Federal Reserve’s December 2025 rate of interest choice, has produced $3.5 million.

The place similar occasions commerce on each platforms, the unfold is substantial. The December Fed choice reveals $120.9 million in quantity on Polymarket versus $3.5 million on Kalshi. The 2028 Democratic Presidential Nominee market reveals $104.3 million on Polymarket versus $1 million on Kalshi.

This hole possible displays Polymarket’s three-year head begin constructing liquidity in high-profile markets. It might additionally replicate consumer composition: Polymarket’s crypto-native viewers—customers depositing USDC and connecting wallets—skews towards bigger place sizes. Kalshi’s fiat on-ramps and Robinhood integration (25-35% of quantity) appeal to a distinct profile.

Valuation context

Kalshi’s $11 billion valuation arrives as the corporate experiences $50 billion in annualized buying and selling quantity, per the New York Occasions—a greater than one-hundred-fold enhance from roughly $300 million the prior 12 months.

Polymarket, which acquired CFTC approval to serve US clients in September, is reportedly in discussions to lift extra capital at a $12 billion to $15 billion valuation, per Bloomberg.

The US market will resolve the class

Each platforms now have US regulatory authorization and world ambitions. Kalshi secured the proper to serve American customers after prevailing in litigation in opposition to the CFTC final 12 months, although it continues to face challenges from state regulators who contend its contracts represent unlawful playing.

The info above suggests American merchants generate extra prediction market quantity than the remainder of the world mixed. Whoever wins the US market will possible outline the class.

Kalshi is betting that regulatory legitimacy and conventional finance integrations—Robinhood, financial institution accounts, potential brokerage partnerships—will pull mainstream customers away from crypto rails. Polymarket is betting that liquidity begets liquidity: merchants go the place the depth is, and three years of gathered market-making in high-profile contracts creates a moat that fiat on-ramps alone can not breach.

Each shall be examined over the subsequent 12 months because the platforms compete for a similar customers for the primary time.

{kind=link}